TL;DR:

- Yacht financing is a secured loan using the vessel as collateral, influencing sale negotiations and buyer affordability.

- Securing pre-approval and understanding loan terms significantly strengthens a buyer’s position and shortens closing times.

Yacht financing is defined as a specialized form of secured lending that uses the vessel itself as collateral, giving buyers access to capital they would otherwise need years to accumulate. The role of yacht financing in sales goes far beyond simple affordability. It shapes negotiation dynamics, determines deal timelines, and directly influences how much vessel a buyer can realistically own without destroying their liquidity. In 2026, marine lenders scrutinize both borrower financials and vessel condition before approving any loan, which means preparation is not optional. Understanding how financing works before you make an offer is the single biggest advantage you can give yourself.

How does yacht financing impact the buying and sales negotiation process?

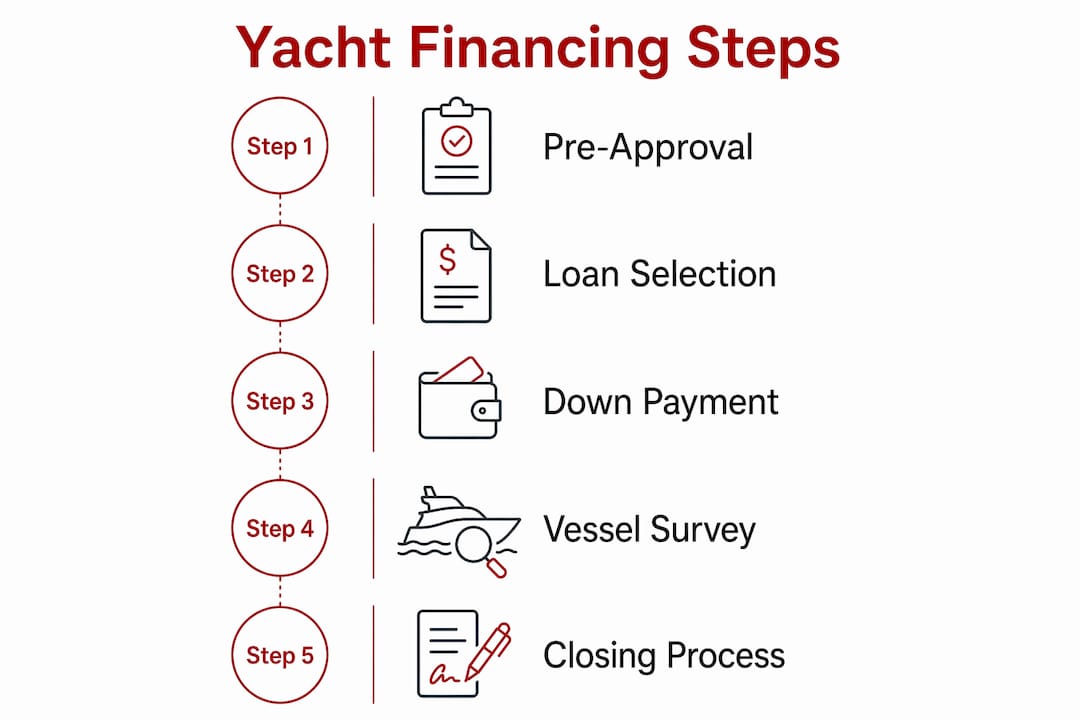

Financing shapes every stage of a yacht transaction, from the first offer to the final closing. Buyers who arrive with a pre-approval letter hold a measurably stronger position than those who have not yet spoken to a lender. Sellers and brokers treat pre-approved buyers as serious, which shortens negotiation cycles and reduces the risk of a deal falling apart at the last moment.

The negotiation dynamic gets more complicated when buyers reveal their financing budget too early. Anchoring on monthly costs signals your ceiling to the seller, which reduces your leverage on the purchase price. The strongest buyers negotiate price first and discuss financing structure only after a figure is agreed upon.

Key factors that financing introduces into the sales process:

- Pre-approval confirms your borrowing capacity and signals commitment to the seller

- Financing contingencies in purchase agreements protect buyers if a loan falls through

- Seller financing is occasionally offered on private sales, typically at shorter terms and higher rates than institutional loans

- Bridge loans allow buyers to purchase a new vessel before selling an existing one, though they carry higher costs and short repayment windows

Conseil de pro : Get pre-approved before you attend any boat show or schedule sea trials. Sellers at shows often have multiple interested parties, and a pre-approval letter can move you to the front of the queue without a single dollar of negotiation.

Closing timelines also depend heavily on financing. A cash buyer can close in days. A financed transaction typically takes 30–60 days once a purchase agreement is signed, largely because lenders require a marine survey, title search, and documentation review before funding. Sellers factor this into their decision when evaluating competing offers.

What are the common yacht financing options and loan terms in 2026?

The marine lending market in 2026 offers several distinct loan structures, each suited to different vessel sizes, buyer profiles, and ownership goals.

Standard secured marine loans require a down payment of 15%–20%, while jumbo marine mortgages on higher-value vessels typically require 20%–30%. That range reflects the lender’s need to protect against depreciation and resale risk. A larger down payment also signals financial strength, which can improve your rate.

Loan terms for larger vessels generally run 10–20 years, while smaller boats are typically financed over 7–12 years. Longer terms reduce monthly payments but increase total interest paid over the life of the loan.

| Loan type | Down payment | Typical term | Best suited for |

|---|---|---|---|

| Standard marine loan | 15%–20% | 10–20 years | Mid-size to large vessels |

| Jumbo marine mortgage | 20%–30% | 15–20 years | High-value or superyacht purchases |

| Bridge loan | Variable | 6–18 months | Buyers selling an existing vessel |

| Refit loan | Variable | 3–7 years | Vessels requiring major refits |

| Portfolio lending | Negotiated | Flexible | High-net-worth buyers with complex assets |

Interest rates in 2026 range from approximately 6.5% to 11%, depending on credit score, vessel age, and loan size. Well-qualified buyers with strong credit and newer vessels access rates in the 6.5%–8.5% range. Older vessels or borrowers with complex income profiles push rates toward the higher end.

Marine loan brokers provide access to multiple specialized lenders and are particularly effective for complex situations, including older vessels, jumbo loans, and non-standard ownership structures. A direct bank relationship works for straightforward purchases, but a broker’s network often produces better terms when your profile does not fit a standard template.

Lenders require proof of income, documented boating experience, and a full vessel survey before approving any loan. Documentation standards have tightened in 2026, so gathering these materials early prevents delays.

What financial considerations beyond monthly payments should buyers factor in?

Monthly loan payments represent only part of what yacht ownership actually costs. Buyers who focus only on the loan figure routinely underestimate their total financial exposure.

Operating costs average approximately 10% of the yacht’s value annually, covering dockage, routine maintenance, insurance, and fuel. That means a $500,000 vessel costs roughly $50,000 per year to operate before you make a single loan payment. That figure is not a worst-case estimate. It is the industry baseline.

Additional upfront costs that buyers frequently underestimate:

- Sales tax varies by state and can add 6%–10% to the purchase price in high-tax jurisdictions

- Marine survey fees typically run $1,000–$3,000 depending on vessel size and are required by lenders before funding

- Insurance premiums on financed vessels are higher because lenders require comprehensive coverage as a loan condition

- Registration and flag fees vary by jurisdiction and ownership structure, and they recur annually

Conseil de pro : Build a 12-month ownership budget before you sign a purchase agreement. Include loan payments, operating costs, insurance, and dockage. If the total exceeds 15%–20% of your annual income, reconsider the vessel size or loan amount.

Lenders evaluate vessel resale liquidity alongside borrower financials, which means the vessel’s brand, condition, and market demand directly affect your loan terms. A well-maintained vessel from a recognized builder commands better financing terms and holds its value more reliably. Overstretching your borrowing capacity on a vessel with weak resale fundamentals creates compounding risk on both sides of the balance sheet.

How to coordinate yacht financing with ownership structure, registration, and tax planning

Yacht financing does not exist in isolation. The ownership structure you choose affects your loan options, your tax position, and your long-term resale strategy. Getting these elements aligned before you close is far easier than restructuring them afterward.

-

Choose your ownership structure early. Many buyers hold yachts through an LLC or trust rather than in their personal name. Corporate ownership structures can simplify liability management and create cleaner financing arrangements, but lenders have specific requirements for entity-held loans. Confirm your lender’s policy before forming the entity.

-

Understand how registration flags affect financing. The flag state under which you register your vessel affects its legal standing, insurance requirements, and resale appeal. Some flags are recognized by major marine lenders as standard; others may require additional documentation or limit your lender options. Reviewing yacht registration tax rules before you commit to a flag saves significant cost and friction.

-

Evaluate the tax deduction opportunity. Loan interest may qualify for a tax deduction if the yacht meets the IRS definition of a second home, which requires sleeping, cooking, and toilet facilities. This deduction can meaningfully reduce the effective cost of financing, but it requires proper documentation and consistent use of the vessel. Confirm eligibility with a tax advisor before assuming the deduction applies.

-

Coordinate your advisors. A yacht purchase at any significant price point requires input from a maritime attorney, a tax advisor, a marine loan broker, and a yacht broker working in concert. Each specialist sees a different dimension of the transaction. Decisions made in one area, such as the ownership entity, directly affect the others, such as the loan structure and the registration flag.

-

Plan for resale from day one. The financing structure you choose today affects how easily you can sell the vessel later. Loans with prepayment penalties, unusual ownership structures, or flags with limited international recognition can complicate a future sale. Build your exit strategy into the purchase decision, not as an afterthought.

Principaux enseignements

Yacht financing directly determines buyer purchasing power, negotiation leverage, and total ownership cost, making it the central variable in any yacht sales transaction.

| Point | Détails |

|---|---|

| Pre-approval strengthens offers | Arrive with lender pre-approval to signal commitment and shorten closing timelines. |

| Down payments range from 15%–30% | Standard marine loans require 15%–20% down; jumbo mortgages require 20%–30%. |

| Operating costs add 10% annually | Budget roughly 10% of vessel value per year for dockage, maintenance, insurance, and fuel. |

| Ownership structure affects loan terms | LLC or trust ownership changes lender requirements and tax treatment; align these early. |

| Registration flag impacts resale | Choose a recognized flag state to preserve financing options and future resale appeal. |

What I have learned about financing and yacht sales after years in this space

The most common mistake buyers make is treating financing as a formality they handle after falling in love with a vessel. By that point, the emotional decision is already made, and the financing terms become something to rationalize rather than evaluate. The sequence should run in the opposite direction.

Working with a specialized marine loan broker before you start shopping gives you a realistic picture of what you can borrow, at what rate, and under what conditions. That knowledge changes which vessels you look at and how you negotiate. Buyers who skip this step routinely overpay or overextend.

The other pattern I see repeatedly is buyers who focus on the monthly payment and ignore the total ownership cost. A vessel that fits your loan payment can still destroy your cash flow if the operating costs were not modeled honestly. The 10% annual operating cost figure is not a scare statistic. It is a planning baseline, and it catches people off guard every time they ignore it.

Vessel surveys deserve more respect than they typically receive. Buyers sometimes treat the survey as a lender requirement to get through rather than as genuine due diligence. A thorough survey protects you from inheriting deferred maintenance that the seller has priced into the asking figure. Prioritize survey outcomes before finalizing any loan amount.

Finally, the registration flag you choose is not a bureaucratic afterthought. It affects your insurance costs, your legal standing in foreign ports, and how easily a future buyer can finance the vessel from you. Treat it as a financial decision, not an administrative one.

— Vesselflag

Vesselflag supports your ownership journey after financing closes

Securing financing is one milestone. Registering your vessel correctly is the next one, and it carries its own legal and financial consequences.

Vesselflag provides yacht owners with clear, compliant registration services across multiple international flag states, including Malta, UK Part 1, San Marino, Palau, and others. Each flag carries different timelines, costs, and compliance requirements that directly affect your insurance terms and resale position. Whether you are registering a newly purchased vessel or restructuring an existing ownership arrangement, Vesselflag walks you through every step. Start with the complete yacht registration guide to understand your options, or review the yacht vs. boat registration distinctions that determine which process applies to your vessel.

FAQ

What is the role of yacht financing in sales?

Yacht financing expands the pool of qualified buyers by making large purchases accessible without full cash payment, which accelerates sales timelines and supports stronger asking prices. It also introduces negotiation dynamics around pre-approval, contingencies, and closing speed.

How much down payment does a yacht loan require?

Standard marine loans require 15%–20% down, while jumbo marine mortgages on higher-value vessels require 20%–30%, depending on the borrower’s credit profile and the vessel’s condition.

What do yacht lenders look at beyond credit score?

Lenders evaluate vessel resale liquidity, the vessel’s brand and condition, proof of income, and documented boating experience. A marine survey is required before any loan is funded.

Can yacht loan interest be tax deductible?

Loan interest may qualify as a deduction if the vessel meets the IRS definition of a second home, requiring sleeping, cooking, and toilet facilities. Confirm eligibility with a qualified tax advisor before claiming the deduction.

What does a yacht finance broker do that a bank cannot?

Marine loan brokers access multiple specialized lenders and can accommodate complex profiles including older vessels, jumbo loans, and entity-held ownership structures that standard bank underwriting typically declines.