TL;DR:

- Charter yacht insurance claims are complex and depend on proper documentation and compliance from the start.

- Operators must accurately disclose commercial use, maintain current certificates, and follow detailed steps for filing claims to ensure recovery.

The charter yacht insurance claim process is the structured sequence of steps a commercial yacht owner or operator must follow from the moment an incident occurs through final claim settlement. Unlike recreational boat claims, charter yacht claims carry added complexity because commercial use, flag state compliance, and crew certification all affect whether your insurer pays. Getting the process right from the first hour determines whether you recover your losses or absorb them yourself.

What does the charter yacht insurance claim process require before you file?

Preparation before an incident is what separates paid claims from denied ones. Charter operators must maintain a specific set of documents that prove both the vessel’s condition and its legal right to operate commercially. Missing even one of these at the time of loss gives underwriters grounds to question coverage.

The core documents every charter operator needs on file include:

- Recent marine survey: Most commercial policies require a survey within the past two to five years. An outdated survey signals deferred maintenance and gives adjusters a reason to dispute seaworthiness.

- Proof of commercial licensing: Your vessel must hold the correct commercial endorsements for the jurisdiction where it operates. A recreational license does not cover charter operations.

- Maintenance logs: Dated, detailed records showing routine engine service, safety equipment checks, and hull maintenance demonstrate that the vessel was kept in good condition.

- Charter agreements: Signed contracts with guests establish the commercial nature of each voyage and confirm that operations were structured and documented.

- Crew certifications: STCW certificates, medical fitness documents, and watch-keeping qualifications for all crew members must be current at the time of any incident.

Compliance with flag state registration, class society requirements, and statutory certification is a strict condition of coverage. Vessels that fail to meet these standards at the time of an incident risk losing coverage entirely, regardless of the nature of the damage.

Verifying that your policy explicitly covers commercial charter use is equally critical. Insurers frequently deny claims when commercial activity was not disclosed or underwritten at policy inception. Investigators routinely examine social media posts, booking platform listings, and charter agreements to detect undisclosed commercial activity.

Pro Tip: Keep a running digital equipment inventory with photos and dated maintenance receipts. Store it in cloud backup so it survives the same incident that damages your vessel.

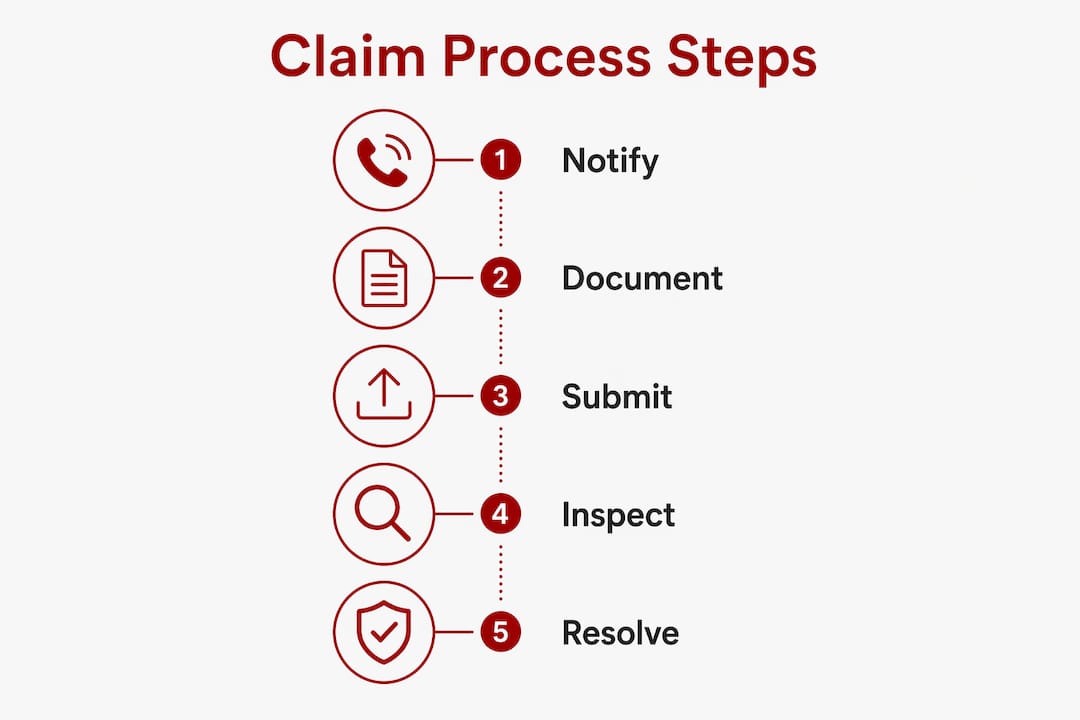

How do you file and manage a charter yacht insurance claim step by step?

The yacht damage claim process follows a clear sequence. Deviating from it, even with good intentions, can reduce or void your payout.

-

Notify your insurer immediately. Prompt loss notification is required by most marine policies. Late reporting undermines claim validity. Call your broker or insurer the same day the incident occurs, even if the full extent of damage is not yet known.

-

Document everything before touching the vessel. Photograph and video all damage from multiple angles. Capture timestamps. Write a factual incident narrative while details are fresh. This initial record becomes your primary evidence.

-

Mitigate further damage with documented temporary measures. Owners must take reasonable steps to prevent additional loss, such as pumping bilges, covering exposed areas, or moving the vessel to a safe berth. Document all mitigation steps with dated photos, receipts, and timestamped notes. Do not begin permanent repairs until the insurer and any appointed surveyor have completed their inspection.

-

Engage a marine surveyor and consider a public adjuster. Your insurer will appoint their own surveyor. You have the right to hire an independent marine surveyor to protect your interests. Marine public adjusters handle investigation, documentation, and negotiation on your behalf, working on contingency fees and communicating with insurers in marine-specific technical language.

-

Submit your claim forms and supporting documentation. This package typically includes the incident report, survey findings, repair estimates, maintenance logs, crew certifications, and charter agreements. Organize documents chronologically and label each one clearly.

-

Manage adjuster communications carefully. The claims adjuster works for the insurer, not for you. Answer questions factually and in writing when possible. Avoid casual verbal statements about the vessel’s condition or history.

-

Review all documents before signing. Insurers may use recorded statements or manipulate the “date of loss” to reduce payouts. Never sign a release or settlement document without independent professional review.

“Offhand recorded comments can be twisted into coverage denial tactics. Professional legal or adjuster advice is critical before you sign anything the insurer prepares.”

Pro Tip: If your claim is denied, request the denial in writing with the specific policy language cited. This is the foundation for any dispute or Civil Remedy Notice filing.

What are the most common pitfalls in charter yacht claims?

Charter yacht claims fail for predictable reasons. Knowing these pitfalls in advance lets you build a claim that is harder to deny.

-

Undisclosed commercial use. This is the single most common denial reason. Recreational insurance does not cover commercial chartering. Underwriters treat charter operations as a materially different risk, and they will investigate thoroughly when a claim is filed.

-

Seaworthiness defenses. Insurers invoke seaworthiness clauses when they can argue the vessel was not fit for the voyage. Gaps in maintenance logs, expired safety equipment, or uncertified crew all feed this defense.

-

Date of loss manipulation. In high-profile disputes, insurers have attempted to split a single damage event into multiple claim dates to apply separate deductibles or sub-limits. Detailed, timestamped incident documentation is your defense against this tactic.

-

Compliance failures at the time of loss. An expired flag state certificate or lapsed class survey at the moment of an incident can void coverage entirely, even when the damage itself is clearly covered under the policy terms.

-

Premature permanent repairs. Completing structural or mechanical repairs before the insurer’s surveyor inspects the vessel destroys evidence and gives adjusters grounds to dispute the scope and cost of damage.

“Insurers often use tactics such as splitting one coverage event into multiple claim dates or invoking seaworthiness clauses to avoid payouts. Seek professional review before responding to any insurer-prepared document.”

The charter yacht liability insurance guide from Vesselflag covers how commercial operators can structure their coverage to reduce exposure to these specific denial tactics.

Best practices for a successful charter insurance claim

The operators who recover the most from claims share a set of consistent habits. These are not complicated. They require discipline and preparation, not luck.

-

Engage a specialist marine broker before a claim happens. Specialist marine insurance brokers clarify complex policy terms and manage insurer communications effectively. Their value during a claim is directly proportional to how well they know your operation before the loss occurs.

-

Keep dated photographic records of the vessel’s condition. Monthly walkaround photos of the hull, engine room, safety gear, and deck equipment create a baseline that proves pre-loss condition. This record is worth more than any written description.

-

Never make permanent repairs before inspection. This rule appears twice in this guide because it is the most commonly broken one. Temporary stabilization is required. Permanent repairs before inspection are not.

-

Read every insurer communication with professional assistance. Policy language in marine insurance is dense and jurisdiction-specific. A phrase that sounds like approval may contain a reservation of rights that limits your recovery.

-

Be fully transparent about charter operations. Disclose all commercial use at policy inception and update your broker whenever your operation changes. Undisclosed changes, such as adding new charter routes or increasing guest capacity, create coverage gaps.

-

Maintain ongoing regulatory compliance. Review your vessel insurance checklist annually to confirm that flag state registrations, class surveys, crew certifications, and safety equipment are all current.

Pro Tip: Schedule a quarterly call with your marine broker to review any changes in your charter operation. Update your policy before the next season, not after the next incident.

Key Takeaways

The charter yacht insurance claim process succeeds when operators combine prompt notification, thorough documentation, and full commercial use disclosure from the first moment of an incident.

| Point | Details |

|---|---|

| Notify immediately | Contact your insurer the same day the incident occurs to preserve claim validity. |

| Document before repairing | Photograph all damage and mitigation steps before any permanent repairs begin. |

| Disclose commercial use | Recreational policies do not cover charter operations; undisclosed use is the top denial reason. |

| Engage professionals early | Marine public adjusters and specialist brokers improve outcomes and protect you from insurer tactics. |

| Maintain compliance always | Expired flag state certificates or lapsed surveys at the time of loss can void coverage entirely. |

What charter operators get wrong about insurance claims

Charter operations carry risks that private yacht owners simply do not face. Every guest who steps aboard creates liability exposure. Every booking platform listing is potential evidence in a coverage dispute. The commercial nature of the operation changes everything about how underwriters assess and respond to claims.

The operators I see struggle most are those who treat their charter yacht like a private vessel with a commercial policy bolted on. That mindset leads to gaps: a maintenance log that stops when charter season starts, crew certifications that lapse mid-season, or a policy that was never updated after the owner added a second vessel to the fleet. These are not obscure technicalities. They are the exact items adjusters check first.

Early engagement with a marine insurance specialist is not optional for charter operators. It is the difference between a claim that settles in weeks and one that drags through dispute for years. The complexity of commercial marine underwriting has increased significantly, and the scrutiny applied to charter claims has grown with it. Operators who stay ahead of compliance requirements, maintain honest communication with their insurers, and prepare their documentation before an incident occurs are the ones who recover quickly and fully. The cost of that preparation is small compared to the cost of a denied claim on a vessel worth hundreds of thousands of dollars.

— Vesselflag

How Vesselflag supports charter yacht registration and compliance

Proper vessel registration is the foundation of any valid charter yacht insurance claim. Without current flag state documentation and compliant commercial registration, your insurer has grounds to deny coverage before the adjuster even reviews the damage.

Vesselflag provides global yacht registration services across flags including Malta, UK Part 1, San Marino, Palau, and others, with each registration structured to meet commercial charter requirements. Operators who register a commercial vessel through Vesselflag receive documentation that satisfies underwriter requirements and supports claim validity from day one. For owners who need to confirm their current registration status, the yacht registration validity guide covers exactly what insurers check and how to stay compliant year-round. Visit Vesselflag to get your registration in order before your next charter season.

FAQ

What is the first step in a charter yacht insurance claim?

Notify your insurer or broker immediately after the incident occurs. Most marine policies require prompt loss notification, and late reporting gives insurers grounds to reduce or deny your claim.

Can a recreational yacht policy cover charter operations?

No. Recreational policies do not cover commercial chartering. Insurers deny claims when commercial use was not disclosed and underwritten at policy inception, and they actively investigate booking records and social media to confirm usage.

What documents do I need to file a yacht insurance claim?

You need a recent marine survey, maintenance logs, crew certifications, charter agreements, proof of commercial licensing, and a detailed incident report with dated photographs. Missing documents give adjusters grounds to dispute coverage.

Can I make repairs before the insurer inspects the vessel?

Temporary repairs to prevent further damage are required and should be documented with photos and receipts. Permanent structural or mechanical repairs must wait until the insurer and any appointed surveyor complete their inspection.

What should I do if my charter yacht claim is denied?

Request the denial in writing with the specific policy language cited. Then engage a marine public adjuster or maritime attorney to review the denial and, if warranted, file a Civil Remedy Notice or pursue professional negotiation with the insurer.