TL;DR:

- The vessel insurance process involves managing multiple policies with different insurers, renewal schedules, and compliance requirements to ensure comprehensive vessel protection. Proper documentation, early renewal planning, and strict adherence to use and cyber regulations are essential for avoiding coverage gaps and claims denials. Regular, organized review and proactive engagement with brokers significantly improve coverage quality and expedite claims settlement.

The vessel insurance process is the structured series of steps boat owners and operators follow to obtain, maintain, and renew the multiple insurance policies required to protect their vessel, crew, and financial interests. Unlike home or auto insurance, marine coverage is not a single policy. It is a stack of distinct covers managed across different insurers, renewal cycles, and compliance requirements. Marine insurance brokers, Protection & Indemnity (P&I) clubs, and specialist underwriters each play a defined role in this process. Understanding how these pieces fit together is what separates owners who get paid on claims from those who discover gaps at the worst possible moment.

What does the vessel insurance process actually cover?

Vessel insurance is structured as a stack of multiple distinct covers, not a single policy, with each layer carrying different insurers and renewal cycles. That distinction matters enormously in practice. Missing one renewal in the stack does not just create a gap in one area. It can expose you to uninsured liability across several risk categories simultaneously.

The seven core policy types every serious boat owner should track are listed below.

| Coverage Type | What It Protects |

|---|---|

| Hull & Machinery (H&M) | Physical damage to the vessel and its equipment |

| Protection & Indemnity (P&I) | Third-party liability, crew injury, pollution |

| War Risk | Loss or damage from war, piracy, or political violence |

| Freight, Demurrage & Defense (FD&D) | Legal costs and contractual disputes |

| Cyber Liability | Losses from cyber incidents affecting vessel systems |

| Strike, Riots & Civil Commotion | Losses from labor disputes or civil unrest |

| Cargo & Charterers’ Liability | Cargo damage and charterer exposure |

Hull & Machinery and P&I are the foundation of any marine policy review. War Risk, Cyber Liability, and FD&D are supplemental but increasingly standard for vessels operating internationally. Cargo and Charterers’ Liability become mandatory the moment you carry paying passengers or freight.

The practical challenge is that these policies often renew on different dates with different underwriters. Centralized tracking is vital to avoid gaps caused by partial renewals or incomplete documentation. Owners who manage each policy in isolation routinely discover mid-season that one cover lapsed while they were focused on renewing another.

What documentation do you need for a marine insurance application?

Underwriters require detailed vessel particulars and operational data to generate accurate quotes and accept risk. Incomplete disclosure does not just slow the process. It can restrict your coverage or void a claim entirely.

The table below outlines the core documentation categories for any marine insurance application or renewal submission.

| Document Category | Specific Requirements |

|---|---|

| Vessel particulars | Type, length, year built, hull material, current condition survey |

| Navigation area | Declared cruising range, ports of call, offshore limits |

| Intended use | Private, charter, racing, commercial, or mixed use |

| Owner and crew | Qualifications, licenses, years of experience, crew certifications |

| Loss record | Five-year claims history with cause and settlement details |

| Safety management | ISM compliance evidence, safety drills log, cyber risk documentation |

The navigation area and intended use fields carry more weight than most owners realize. Misdeclaration of vessel use is one of the most common causes of denied claims. A vessel declared for private use that is actively chartering operates outside its policy terms. The underwriter has grounds to reject any claim arising from that activity.

Many insurers also require formal underwriting questionnaires specific to vessel type and supplemental covers such as theft prevention statements or cyber risk declarations. These forms are not optional extras. They are part of the binding process.

Pro Tip: Prepare your documentation package at least 90 days before renewal. A complete, organized submission gives underwriters confidence and gives you negotiating leverage on premium and deductibles.

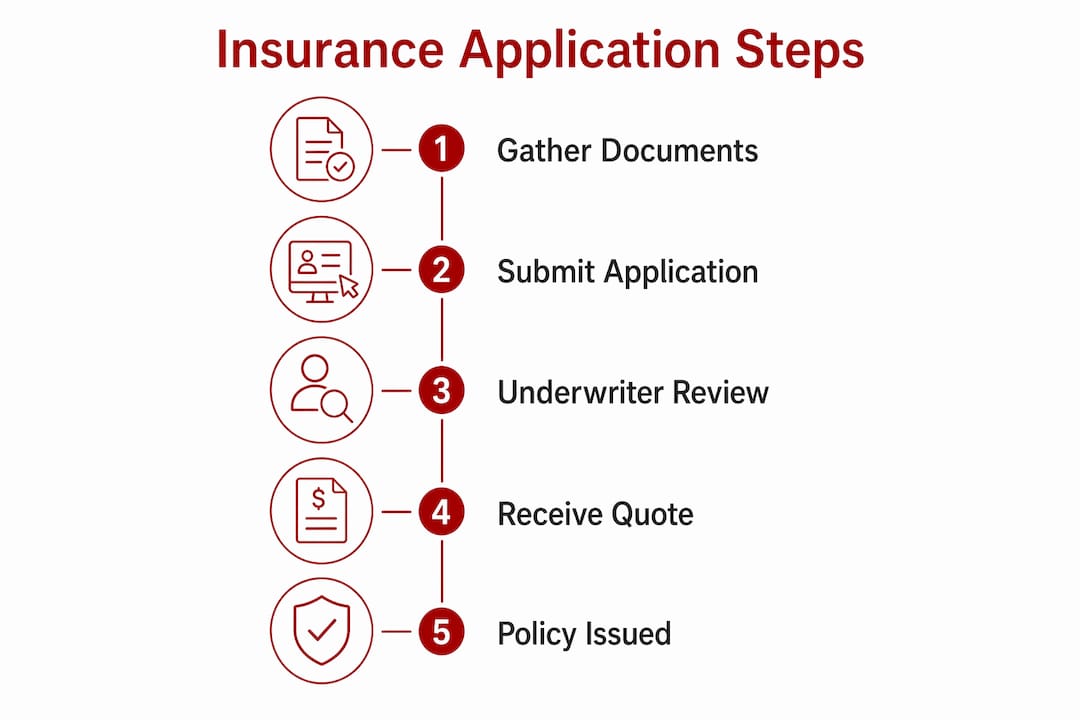

How does the vessel insurance renewal timeline work?

The 90-day renewal cycle is the industry standard for managing vessel insurance renewals without rushed submissions or last-minute coverage gaps. Compressing the entire process into the final 30 days before expiry consistently produces higher premiums and weaker policy terms.

Here is the phased approach that professional marine insurance brokers recommend:

-

T-90 (90 days out): Loss review. Pull your five-year claims history and identify any trends, open claims, or incidents that need explanation. Underwriters will ask. Having a prepared narrative is far better than scrambling to explain a claim on short notice.

-

T-75 (75 days out): Submission pack. Assemble all vessel particulars, updated surveys, crew credentials, safety management evidence, and cyber compliance documentation. Submit to your broker for distribution to underwriters.

-

T-60 (60 days out): Quotes received. Review competing quotes from multiple underwriters. Compare not just premium but deductibles, exclusions, navigation limits, and endorsement options. A lower premium with a broader exclusion clause is rarely a better deal.

-

T-30 (30 days out): Negotiation. Use competing quotes as leverage. Negotiate on premium, deductibles, and specific endorsements relevant to your operations. This is also the time to confirm War Risk and supplemental covers are aligned with your H&M renewal date.

-

T-0 (binding): Policy confirmation. Confirm all covers are bound, certificates issued, and documentation filed. Verify that every policy in your stack is active before the prior period expires.

Renewal underwriting packs routinely require safety management and cyber compliance evidence alongside loss data. This is not just form filling. It requires coordination across your operations team, your broker, and sometimes your flag state authority.

Pro Tip: Set calendar alerts for each phase of the renewal cycle across every policy in your stack. A single missed alert on a War Risk renewal can leave your vessel uninsured in high-risk waters without you knowing it.

How do you file and manage a marine insurance claim?

Marine insurance claims require notification within 24 to 48 hours of discovery to preserve your coverage rights. Delayed notification gives insurers grounds to reduce or deny the claim entirely. Written notice is always preferable to a phone call alone.

Follow these steps from the moment an incident occurs:

-

Notify your insurer and broker immediately. Send written notice within 24 hours. Include the vessel name, policy number, date, location, and a brief factual description of the incident.

-

Preserve all operational evidence. Operational logs and protest reports are the primary evidence base for surveyor investigations. Do not alter, delete, or summarize logs. Preserve photographs, AIS data, engine room records, and any communications related to the incident.

-

Request surveyor appointment. Your insurer will appoint a marine surveyor. Cooperate fully and provide access to the vessel and all records. The surveyor’s report is the foundation of the claims adjustment process.

-

Assemble your documentation package. This includes the master’s log, protest report, photographs, repair estimates, crew statements, and any third-party correspondence. A complete package submitted early accelerates settlement.

-

Follow up on investigation milestones. Claims resolution typically takes two to six months depending on complexity. Complex total loss or liability claims can extend well beyond that. Track progress actively and maintain written records of all insurer communications.

Common pitfalls that delay or kill claims include:

- Failing to issue a formal protest report after a grounding or collision

- Allowing unauthorized repairs before the surveyor inspects the damage

- Submitting incomplete documentation that requires multiple follow-up requests

- Operating outside declared navigation limits at the time of the incident

Early and written claim notification enables insurer coordination, faster surveyor appointment, and improved evidence quality for claims adjustment. Owners who treat notification as a formality rather than a strategic step consistently receive slower settlements and lower payouts.

What compliance challenges affect the vessel insurance process?

Compliance failures are the most preventable cause of coverage restrictions and claim denials in the yacht insurance process. Three areas generate the most underwriting problems for boat owners and operators.

Navigation area and use disclosure is the most common source of disputes. Underwriters price and structure policies based entirely on declared use. The premium difference between private use and commercial chartering is material. Operating outside declared terms does not just affect the incident in question. It can void the entire policy retroactively.

Cyber risk management is now a mandatory compliance requirement, not an optional upgrade. IMO MSC.428(98) requires cyber risk management to be embedded in a vessel’s Safety Management System and audited during ISM code compliance reviews. Non-conformance at audit can trigger corrective actions that directly affect insurance renewal. Underwriters increasingly require documented cyber risk procedures as part of the submission pack.

Sanction screening and reinsurance transparency matter more than most private owners expect. Vessels operating in sanctioned regions or under opaque ownership structures face serious problems at port authority inspections and during claims investigations. Insurers and reinsurers both conduct sanction checks. A vessel that cannot produce verifiable, clean documentation faces coverage denial regardless of premium payment history.

Pro Tip: Review your vessel’s insurance documentation checklist annually, not just at renewal. Operational changes like adding a charter program or extending your cruising range mid-season require immediate policy endorsement, not a note for next year.

Key takeaways

The vessel insurance process succeeds when owners treat it as a structured, multi-policy discipline with defined phases, complete documentation, and proactive compliance management rather than a single annual transaction.

| Punkt | Einzelheiten |

|---|---|

| Insurance is a policy stack | Seven distinct covers require separate tracking, renewal dates, and insurer coordination. |

| Documentation drives underwriting | Complete vessel particulars, accurate use disclosure, and cyber compliance evidence determine quote quality and coverage terms. |

| 90-day renewal cycle | Starting the renewal process 90 days out with phased milestones reduces cost and prevents coverage gaps. |

| Claim notification is time-critical | Written notice within 24 to 48 hours of an incident is required to preserve coverage rights. |

| Compliance is non-negotiable | IMO cyber requirements and accurate navigation declarations directly affect underwriting acceptance and claims validity. |

What working with vessel owners has taught us about insurance

Most coverage problems we see at Vesselflag trace back to one root cause: owners treating vessel insurance as a single annual event rather than an ongoing operational discipline. The multi-policy reality of marine coverage means that a gap in one layer, say a lapsed War Risk certificate on a vessel transiting the Red Sea, creates exposure that no amount of H&M coverage can fix.

The owners who consistently get better terms and faster claim settlements share two habits. They start their renewal cycle early, and they maintain documentation that is audit-ready year-round, not just assembled in a panic before submission. A well-organized vessel insurance renewal timeline is not bureaucratic overhead. It is the single most effective tool for negotiating with underwriters from a position of strength.

Cyber risk integration has changed the underwriting conversation significantly in the past two years. Underwriters now ask for documented cyber procedures as a standard part of the submission pack. Owners who have embedded cyber risk management into their Safety Management Systems get better terms. Those who treat it as a checkbox exercise get exclusions.

The broker relationship also matters more than most owners acknowledge. A broker who knows your vessel’s history, your operational patterns, and your risk tolerance can advocate for you in ways that a direct online application never can. Build that relationship before you need it, not during a claim.

— VesselFlag

How Vesselflag supports your vessel insurance documentation

Managing a multi-policy vessel insurance stack across different insurers, renewal dates, and compliance requirements is operationally demanding. Vesselflag’s platform centralizes Hull & Machinery, P&I, War Risk, and supplemental cover documentation in one place, with phase-based renewal alerts that trigger at T-90, T-75, T-60, T-30, and T-0 for every policy in your stack. Audit-ready certificate generation and pre-assembled claims documentation packages mean you are never scrambling when an insurer or port authority asks for proof of coverage. For owners who also need to confirm that their yacht registration is valid before submitting an insurance application, Vesselflag handles both in a single workflow. Start with a clean, compliant foundation and keep it that way.

FAQ

What is the vessel insurance process?

The vessel insurance process is the structured series of steps for obtaining, maintaining, and renewing the multiple insurance policies that cover a boat or ship. It includes documentation preparation, underwriter submission, policy negotiation, binding, and ongoing compliance management.

How many policies does a vessel typically need?

Most vessels require at least two to three core policies, typically Hull & Machinery, P&I, and War Risk, with additional covers for cyber liability, FD&D, and cargo depending on vessel use and operating area.

How long does a marine insurance claim take to settle?

Marine claims resolution typically takes two to six months depending on complexity. Straightforward hull damage claims resolve faster, while total loss or third-party liability claims can take considerably longer.

What happens if I misdeclare my vessel’s use?

Misdeclaring vessel use gives underwriters grounds to deny claims and potentially void the policy. Operating a vessel declared for private use as a charter vessel is one of the most common causes of coverage denial.

When should I start the vessel insurance renewal process?

Start 90 days before your policy expiry date. This gives you time to review loss history, assemble documentation, receive competing quotes, and negotiate terms without the cost and risk that come from last-minute submissions.