TL;DR:

- Proper preparation and documentation are essential for accurate boat insurance coverage.

- Regular policy reviews and honest disclosure prevent claim denials and coverage gaps.

- Insurance costs depend on vessel value, usage, location, and operator experience.

Imagine returning to the marina after a weekend trip to find your boat has been sideswiped by another vessel. The repair bill comes in at $18,000. No insurance. That scenario plays out more often than most boat owners expect, and the financial hit can be devastating. Setting up the right boat insurance is not just about ticking a compliance box. It is about protecting your investment, your passengers, and your peace of mind. This guide walks you through everything: what to prepare, how to buy, which coverages matter, what it costs, and how to stay compliant long after you sign the policy.

Índice

- What you need before buying boat insurance

- Step-by-step process to set up boat insurance

- Understanding coverage types and key options

- Factors affecting cost and special cases

- How to verify your insurance and maintain compliance

- Our perspective: What most guides miss about boat insurance setup

- Make vessel protection and compliance easy with Vessel Flag

- Frequently asked questions

Principais conclusões

| Ponto | Detalhes |

|---|---|

| Preparation is key | Gather your boat’s details, value, and legal requirements before shopping for insurance. |

| Choose the right coverage | Understand the pros and cons of agreed value versus actual cash value and select coverage that fits your needs. |

| Shop around for quotes | Compare offers from multiple carriers and look for available discounts to get the most value. |

| Review policies annually | Update your insurance each year to reflect changes in usage, value, and compliance requirements. |

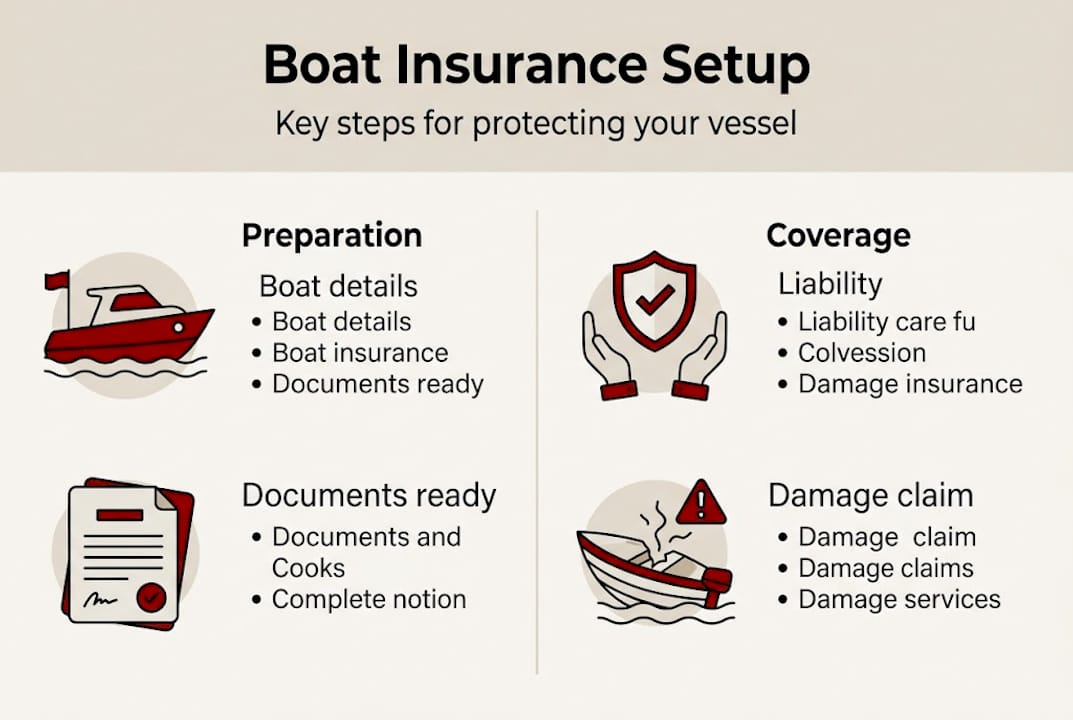

What you need before buying boat insurance

Before you request a single quote, you need to gather the right information. Skipping this step leads to inaccurate quotes, coverage gaps, and sometimes outright claim denials. Think of it as doing your homework before a major purchase.

Here is what every insurer will ask for:

- Vessel details: Make, model, year, hull material, and length

- Current market value: Use a reliable boat value assessment to establish a defensible number

- Intended use: Recreational, charter, racing, or commercial operations each carry different risk profiles

- Storage location: Kept at a marina, on a trailer, or in a boatyard affects your premium significantly

- Operator history: Years of experience, prior claims, and any boating safety certifications

- Financing details: If you have a lender, they will likely require specific coverage minimums

One factor many first-time buyers overlook is the marine survey. For boats over 15 years old, most insurers require a professional inspection before issuing a policy. The survey confirms the vessel’s condition, identifies deferred maintenance, and validates the stated value. Skipping it is not an option with older boats.

You also need to understand any local compliance requirements. Most US states do not legally mandate boat insurance, but Arkansas requires liability coverage for vessels over 50 horsepower, and Utah has its own requirements. Beyond state law, marinas and lenders almost always require proof of coverage before you can dock or finance. Our boat insurance overview breaks down what those requirements typically look like across different jurisdictions.

O step-by-step process starts with a thorough assessment of your boat’s type, value, usage, and location. Getting these details right upfront saves time and prevents surprises later.

| Document needed | Why it matters |

|---|---|

| Vessel registration | Confirms legal ownership and flag state |

| Marine survey (15+ years) | Validates condition and insurable value |

| Prior insurance history | Affects premium and eligibility |

| Safety certifications | Can qualify you for discounts |

| Lender or marina requirements | Sets minimum coverage thresholds |

Pro Tip: Pull your vessel’s title and registration documents before contacting any insurer. Having them ready speeds up the quote process and signals to underwriters that you are a prepared, low-risk client.

For a deeper look at what coverage should include, the yacht insurance coverage essentials guide is a solid starting point.

Step-by-step process to set up boat insurance

With your documents ready, here is how the actual purchase process works from start to finish.

- Assess your boat details. Confirm the make, model, year, value, and intended use. Be precise. Inaccurate details can void a claim.

- Determine your coverage needs. Decide which risks matter most: hull damage, liability, towing, or all of the above. Your usage pattern drives this decision.

- Choose a valuation method. Agreed value or actual cash value (ACV). This is one of the most important decisions you will make.

- Get at least three quotes. Rates vary significantly between insurers. Compare not just price but exclusions, deductibles, and claim service reputation.

- Review add-ons. Towing coverage, personal effects, fishing equipment, and emergency assistance are often sold separately.

- Complete the marine survey if required. For older vessels, this is non-negotiable.

- Purchase the policy and confirm documentation. Get your certificate of insurance and any additional insured endorsements your marina or lender needs.

- Review annually. Your boat’s value, usage, and location can change. Your policy should reflect that.

O full insurance setup process follows this same logic: assess, determine needs, compare quotes, consider surveys, and review every year.

The valuation method deserves extra attention. Here is a direct comparison:

| Valuation type | How it pays | Best for |

|---|---|---|

| Agreed value | Full agreed amount, no depreciation | Newer boats, higher-value vessels |

| Actual cash value (ACV) | Market value minus depreciation | Older boats, budget-conscious owners |

Pro Tip: If your boat is less than 10 years old or has significant upgrades, agreed value is almost always worth the slightly higher premium. The difference in payout after a total loss can be tens of thousands of dollars.

If you operate a commercial vessel, the process has additional layers. The guide on how to register a commercial vessel covers the compliance requirements that intersect with your insurance obligations. The Boat Insurance 101 primer is also a useful reference for understanding foundational terms before you speak with an underwriter.

Understanding coverage types and key options

Not all boat insurance policies are built the same. Understanding what each coverage type actually does helps you build a policy that fits your real risk exposure.

O core coverage categories include:

- Liability coverage: Pays for bodily injury or property damage you cause to others. Limits typically range from $50,000 to $1 million.

- Hull and collision: Covers physical damage to your own vessel from accidents, grounding, or collision.

- Comprehensive: Protects against non-collision events like theft, fire, vandalism, and weather damage.

- Towing and assistance: Covers emergency towing if you break down on the water. Often undervalued until you need it.

- Uninsured boater coverage: Pays your costs if another boater causes damage and has no insurance.

- Medical payments: Covers medical expenses for you and your passengers regardless of fault.

“For newer boats, agreed value policies provide far greater financial certainty. When a vessel is totaled, the last thing you want is a depreciation argument with your insurer.” This is why agreed value pros and cons are worth understanding before you sign anything.

Liability is the coverage most marinas and lenders focus on. A $300,000 minimum is common for marina berthing agreements, and some require up to $1 million. Do not assume the state minimum is enough. It rarely is.

To avoid the trap of being dangerously underinsured, review the detailed breakdown on avoiding underinsurance. Studies show that up to 40% of recreational boats are underinsured, meaning owners would face significant out-of-pocket costs even with a policy in place.

Factors affecting cost and special cases

Premiums are not random. Insurers use a specific set of variables to calculate your rate, and understanding them helps you plan your budget and find legitimate savings.

| Vessel value | Estimated annual premium |

|---|---|

| Under $20,000 | $200 to $400 |

| $20,000 to $100,000 | $400 to $1,500 |

| $100,000 to $500,000 | $1,500 to $7,500 |

| Over $500,000 | $10,000 to $50,000+ |

Premium benchmarks typically run 1 to 1.5% of hull value annually, with discounts available for safety training, lay-up periods, and operator experience.

The main cost drivers include:

- Boat age and condition: Older vessels cost more to insure without a clean survey

- Geographic location: Coastal areas prone to hurricanes carry higher premiums

- Operator experience: More years on the water, lower rates

- Intended use: Racing and charter use spike premiums significantly

- Claims history: Prior claims raise your risk profile

- Storage method: Dry storage or a secure boatyard lowers risk versus open water mooring

Special cases worth knowing: hurricane coverage often requires specific precautions or exclusions in high-risk zones. Racing is typically excluded from standard policies and requires a separate endorsement. Off-season lay-up discounts can reduce premiums by up to 60% if you store your boat out of the water during winter months.

For a full breakdown of what drives cost factors in maritime services, that resource covers the broader picture. The cost benchmarks guide also provides useful comparisons across vessel types.

Pro Tip: Completing a US Coast Guard or BoatUS safety course can qualify you for premium discounts with most major insurers. Bundling your boat policy with your home or auto insurance is another easy way to cut costs without reducing coverage.

You can also explore insurance service options to see what coverage packages are available for different vessel types and usage profiles.

How to verify your insurance and maintain compliance

Buying the policy is only half the job. Verifying it is active and maintaining compliance is an ongoing responsibility.

Here is how to confirm your coverage is actually working:

- Request your certificate of insurance (COI). This is the standard document marinas, lenders, and port authorities will ask for.

- Check the named insured and vessel details. Errors here can cause claim denials.

- Confirm additional insured endorsements if required by your marina or lender.

- Verify the coverage dates and renewal terms. Lapses in coverage can void your marina agreement.

- Store digital and physical copies of all policy documents on and off the vessel.

Your annual review checklist should include:

- Has the boat’s market value changed significantly?

- Have you made upgrades or modifications that increase replacement cost?

- Has your usage changed (added charter trips, changed home port)?

- Are there new add-ons or equipment worth insuring separately?

- Have any state requirements changed in your home state?

One area that catches owners off guard is seaworthiness. If your vessel is not properly maintained and a claim is filed, the insurer can deny it on grounds that the boat was not seaworthy at the time of loss. Non-disclosure of known defects is treated the same way. Be honest in your application.

The guidance on annual insurance reviews explains why reviewing your policy for changes in value, usage, and location every year is not optional if you want real protection.

Pro Tip: Set a calendar reminder 60 days before your policy renewal date. That window gives you enough time to get competing quotes, update your vessel details, and negotiate better terms without rushing.

Our perspective: What most guides miss about boat insurance setup

Most boat insurance guides stop at the steps. They tell you what to buy but not what to watch out for after you buy it. That gap is where real financial pain lives.

The biggest mistake we see is owners treating insurance as a one-time task. They buy a policy, file it away, and forget it exists until something goes wrong. By then, the boat has been upgraded, the usage has changed, or the value has shifted, and the policy no longer reflects reality. That mismatch is how a $90,000 boat ends up with a $55,000 payout.

Conventional advice also underplays the importance of honest disclosure. Insurers are very good at finding reasons to deny claims, and any inconsistency between your application and the facts at the time of loss is a red flag they will pursue. The compliance challenges in maritime registration mirror this pattern: small documentation errors create outsized problems.

Our strong recommendation is to treat your annual policy review as seriously as you treat your vessel’s maintenance schedule. Update values, disclose changes, and never chase a lower premium at the expense of real coverage.

Make vessel protection and compliance easy with Vessel Flag

Setting up boat insurance correctly takes preparation, the right documents, and a clear understanding of what you actually need. That is a lot to manage alongside vessel registration and compliance obligations.

Em VesselFlag.com, we help boat owners and operators handle both sides of the equation. From boat insurance solutions tailored to your vessel type and usage, to practical guidance on insuring your boat without leaving gaps in your coverage, we make the process straightforward. Need help with registration too? Our registration guidance covers everything from flag selection to compliance documentation. Get started today and protect what you have built.

Frequently asked questions

Is boat insurance required by law in the US?

Boat insurance is not legally required in most US states, but Arkansas mandates it for vessels over 50 horsepower and Utah has its own rules. Marinas and lenders typically require $300,000 to $1 million in liability coverage regardless of state law.

What’s the main difference between agreed value and actual cash value policies?

Agreed value pays the full pre-set amount on a total loss with no depreciation deducted, while actual cash value subtracts depreciation from the payout, often leaving you with significantly less than replacement cost.

How much does boat insurance cost on average?

Annual premiums run 1 to 1.5% of hull value, which translates to roughly $200 to $600 for small boats and up to $50,000 or more for large yachts valued at $1 million and above.

Can I get discounts on my boat insurance policy?

Yes. Discounts for safety courses, bundling with home or auto policies, multi-boat ownership, and off-season lay-up storage can reduce your premium meaningfully, with lay-up discounts reaching up to 60% in some cases.

How often should I review my boat insurance policy?

You should review your policy annually or immediately after any change in your boat’s value, usage pattern, home port, or major equipment upgrades to ensure your coverage still matches your actual exposure.