Many yacht owners believe their insurance policy covers everything that can go wrong on the water, only to discover critical gaps when filing a claim. Understanding exactly what a yacht insurance policy includes and excludes can save you tens of thousands of dollars in unexpected costs. This comprehensive guide breaks down every essential aspect of yacht insurance in 2026, from standard hull coverage to specialized protection and indemnity insurance. You’ll learn what policies typically include, how premiums and deductibles work, what optional coverages matter most, and how to obtain and manage your policy effectively to avoid costly mistakes.

Inhaltsübersicht

- What A Yacht Insurance Policy Covers: Standard And Optional Protections

- Understanding Yacht Insurance Costs, Premiums, And Deductibles

- Protection And Indemnity Insurance: Filling Coverage Gaps In Yacht Policies

- How To Obtain And Manage Yacht Insurance Policies Effectively

- Secure Your Yacht’s Future With Expert Registration And Insurance Services

- Häufig gestellte Fragen

Key takeaways

| Punkt | Einzelheiten |

|---|---|

| Comprehensive vessel protection | Yacht insurance covers hull damage, equipment, liability, personal effects, and medical payments specifically designed for high-value recreational vessels. |

| Flexible coverage options | Policies combine standard protections with optional add-ons tailored to your yacht’s type, cruising regions, and operational needs. |

| Cost structure matters | Premiums typically represent 1-2% of vessel value while deductibles range from 1-3% of hull value, significantly impacting your financial exposure. |

| P&I fills critical gaps | Protection and indemnity insurance addresses third-party risks like environmental damage and cargo liability that traditional policies exclude. |

| Active management prevents disputes | Annual policy reviews, proper documentation, and timely claim notices help avoid coverage denials and ensure adequate protection. |

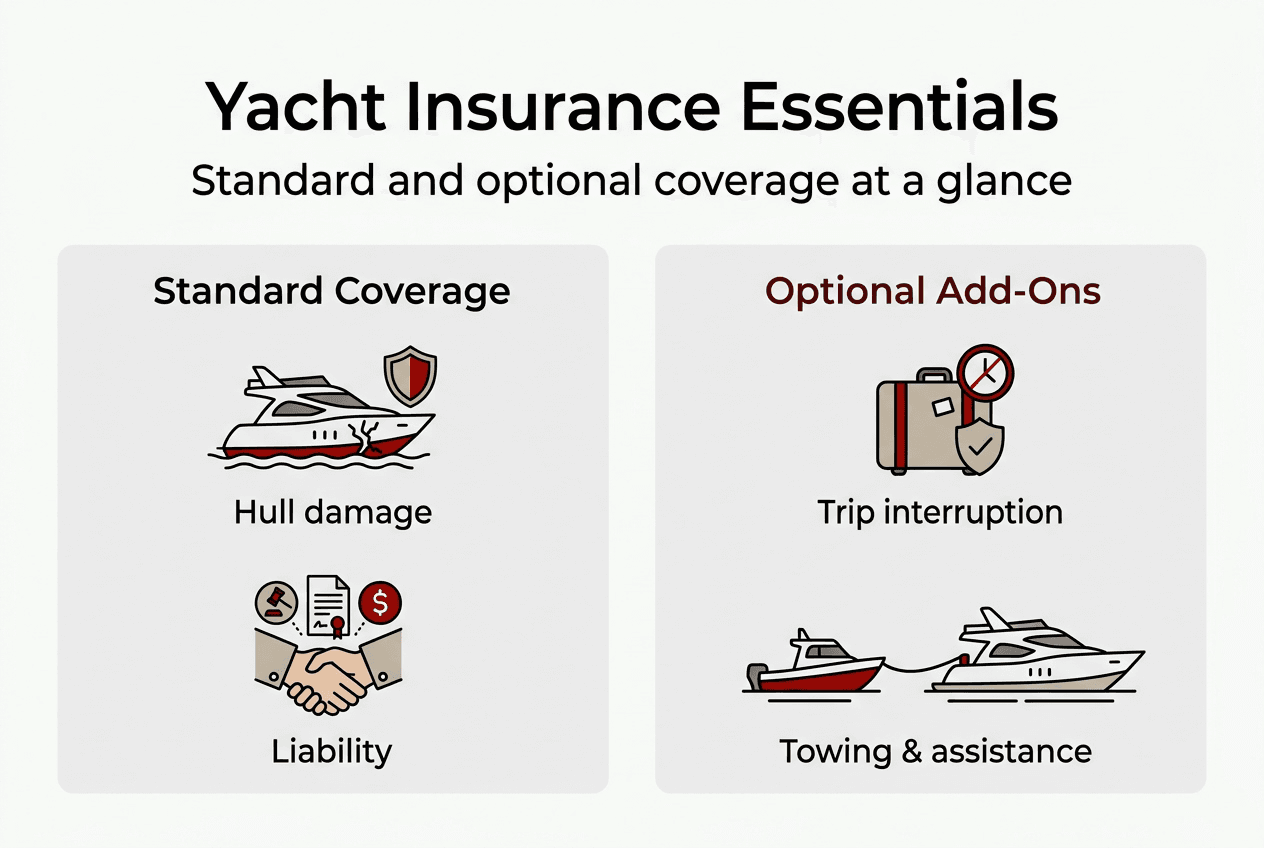

What a yacht insurance policy covers: standard and optional protections

Yacht insurance provides specialized marine coverage to protect high-value recreational vessels, their owners, and passengers from financial losses due to accidents, damage, liability, and other risks unique to yachting. Unlike standard boat insurance, yacht policies recognize the substantial investment and complex operational requirements of luxury vessels, offering more comprehensive protection tailored to sophisticated maritime activities.

Standard hull and equipment coverage forms the foundation of every yacht policy. Insurers typically use an agreed-value basis, meaning you and your insurer establish the yacht’s value upfront, guaranteeing full reimbursement up to that amount if the vessel becomes a total loss. This approach eliminates disputes about depreciation during claims and provides certainty about your financial protection.

Standard yacht insurance includes several essential protections beyond hull damage:

- Personal effects and onboard gear coverage protects belongings stored on your yacht

- Medical payments coverage handles injuries to passengers regardless of fault

- Uninsured boater coverage protects you when other vessels lack adequate insurance

- Legal liability coverage addresses claims from third parties for bodily injury or property damage

- Wreck removal coverage pays for salvage and removal if your yacht sinks or becomes a navigation hazard

Modern policies increasingly include worldwide navigation limits, allowing you to cruise internationally without geographic restrictions. This flexibility matters for owners who enjoy extended voyages or seasonal relocations between different cruising grounds. Understanding your yacht insurance coverage essentials helps ensure you select appropriate geographic protections.

Optional coverages let you customize protection based on your specific needs. Popular add-ons include trip interruption insurance, which reimburses expenses when mechanical failures or covered events force you to cut voyages short. Weather-related coverages extend protection for hurricane damage in vulnerable regions. Jet ski and tender coverage protects auxiliary watercraft you carry aboard.

Towing and assistance coverage proves invaluable when mechanical issues strand you at sea. Trailer coverage protects the equipment used to transport your yacht over land. Captain and crew liability coverage becomes essential if you employ professional operators, protecting against employment-related claims and operational errors.

Some regions require specialized add-ons. Mexico watercraft liability coverage, for example, addresses unique legal requirements for cruising Mexican waters. Working with an experienced broker helps identify which optional coverages match your cruising patterns and risk exposure.

Understanding yacht insurance costs, premiums, and deductibles

Annual premiums for yacht insurance typically range from 1-2% of the yacht’s value, varying based on region and vessel type. A $2 million yacht might cost $20,000 to $40,000 annually to insure, though rates fluctuate significantly based on multiple factors. Understanding these cost drivers helps you anticipate expenses and potentially reduce premiums through smart risk management.

Premium calculations consider your yacht’s characteristics, your experience level, and operational factors. Newer vessels with advanced safety systems typically qualify for lower rates than older yachts lacking modern equipment. Your cruising region dramatically impacts costs, with hurricane-prone areas commanding substantially higher premiums than protected inland waters.

Yacht insurance deductibles typically range from 1% to 3% of the insured hull value. On a $2 million yacht with a 2% deductible, you’d pay the first $40,000 of any claim out of pocket before insurance coverage begins. This structure means even minor incidents can result in substantial personal expenses, making preventive maintenance and careful operation financially prudent.

Named storm deductibles represent a critical cost consideration often overlooked by new yacht owners. These specialized deductibles apply specifically to hurricane and tropical storm damage, typically ranging from 5% to 10% of hull value. In hurricane-prone regions, a 5% named storm deductible on a $2 million yacht means $100,000 out of pocket before insurance pays anything for storm damage.

| Deductible Type | Typical Percentage | Example Cost ($2M Yacht) | When It Applies |

|---|---|---|---|

| Standard hull damage | 1-3% | $20,000-$60,000 | Most covered incidents |

| Named storm | 5-10% | $100,000-$200,000 | Hurricane/tropical storm damage |

| Theft/vandalism | 2-5% | $40,000-$100,000 | Criminal acts |

| Machinery breakdown | 1-2% | $20,000-$40,000 | Mechanical failures |

Several factors influence your premium rates and deductible options:

- Yacht age, condition, and safety equipment installations

- Your boating experience, training certifications, and claims history

- Primary mooring location and typical cruising areas

- Whether you employ professional crew or operate the vessel yourself

- Security measures like tracking systems and marina security

- Seasonal usage patterns and winter storage arrangements

Understanding boat registration cost factors alongside insurance expenses helps you budget comprehensively for yacht ownership. Many owners discover that avoiding underinsurance for boats requires regular policy reviews as vessel values and replacement costs change over time.

Pro Tip: Treat your deductible as a financial risk management tool rather than an annoyance. Choosing a higher deductible reduces premiums substantially while encouraging you to invest in preventive maintenance and safety systems that ultimately reduce claim frequency. Many experienced owners find that the premium savings over several years offset occasional deductible payments.

Protection and indemnity insurance: filling coverage gaps in yacht policies

Protection and indemnity insurance covers third-party risks that traditional insurers are reluctant to insure, such as damage to cargo, war risks, and environmental damage. While standard yacht policies provide solid hull and basic liability coverage, they often exclude or severely limit protection for complex third-party claims that can generate catastrophic financial exposure.

P&I insurance originated in the commercial shipping industry but increasingly applies to large private yachts, especially those over 80 feet or operating in international waters. The coverage addresses liability scenarios that standard yacht policies typically exclude or cap at inadequate limits. Understanding these gaps helps you avoid discovering insufficient coverage only after a serious incident occurs.

Common risks covered by P&I insurance include cargo damage when you transport goods or personal items for others, even informally. War risks extend protection to conflict zones and piracy-prone regions where standard policies exclude coverage entirely. Pollution and environmental damage coverage addresses the potentially enormous costs of fuel spills, sewage discharge violations, or damage to protected marine ecosystems.

Crew injury and illness claims represent another critical P&I coverage area. While standard policies may cover medical payments, they often exclude employment-related claims, repatriation costs, and long-term disability expenses for professional crew members. P&I insurance fills these gaps, protecting you from claims that can easily reach millions of dollars.

A P&I club is a mutual insurance association that provides risk pooling, information and representation for its members. Rather than purchasing coverage from a traditional insurance company, you join a club alongside other yacht owners, sharing risk collectively. This mutual structure often provides more comprehensive coverage at competitive rates compared to conventional insurance markets.

| Coverage Type | Traditional Yacht Insurance | P&I Insurance |

|---|---|---|

| Hull and machinery damage | Comprehensive coverage | Not typically covered |

| Third-party property damage | Limited coverage with caps | Extensive coverage |

| Environmental/pollution liability | Excluded or minimal | Comprehensive protection |

| Crew injury and illness | Basic medical payments only | Full employment liability |

| Cargo damage | Usually excluded | Covered |

| Risiken durch Krieg und Piraterie | Excluded | Available coverage |

Key benefits and considerations of P&I club membership include:

- Mutual risk sharing often provides broader coverage than commercial insurance markets

- Access to specialized maritime legal expertise and claims handling

- Collective financial responsibility means all members share in club losses

- Entry requirements may include vessel surveys and operational standards

- Annual calls (additional premiums) may be assessed if club losses exceed reserves

- International recognition and acceptance at ports worldwide

Your yacht insurance coverage essentials should include evaluation of whether P&I coverage makes sense for your vessel and operations. Larger yachts, those with professional crew, and vessels cruising internationally almost always benefit from P&I protection. Smaller yachts operating primarily in domestic waters may find standard policies sufficient.

Pro Tip: Review your cruising plans annually and ensure your policy includes appropriate P&I coverage before entering higher-risk regions. Many standard policies exclude coverage in certain geographic areas or during specific seasons, leaving you exposed precisely when you need protection most. Exploring boat insurance options with experienced maritime brokers helps identify coverage gaps before they become expensive problems.

How to obtain and manage yacht insurance policies effectively

Securing appropriate yacht insurance requires systematic preparation and clear communication with insurers and brokers. The process typically unfolds in five distinct steps, each requiring specific documentation and attention to detail. Understanding this timeline helps you plan ahead, especially when purchasing a new yacht or switching insurers.

First, conduct initial inquiry and needs assessment. Contact specialized yacht insurance brokers who understand the unique requirements of high-value recreational vessels. Provide basic information about your yacht, including make, model, year, value, and intended use. Discuss your experience level, cruising plans, and any special requirements like professional crew or international voyages.

Second, request detailed quotes from multiple insurers. Insurance setup aligns with standard ownership and survey timelines, with initial quotes provided within 1-3 business days. Compare not just premium costs but also coverage limits, deductibles, exclusions, and optional coverages available. Pay particular attention to geographic limits and any seasonal restrictions that might affect your cruising plans.

Third, submit required documentation for underwriting review. Insurers typically require a recent marine survey conducted by an accredited surveyor, comprehensive maintenance records demonstrating proper care, and proof of ownership through title documentation or purchase agreements. Additional documents may include captain credentials if you employ professional operators, safety equipment inventories, and photographs of the vessel’s condition.

Fourth, complete the underwriting process. Underwriting review typically takes 1-2 weeks, requiring survey and maintenance records. Underwriters assess risk based on vessel condition, your experience, intended use, and operational factors. They may request additional information or require specific safety upgrades before approving coverage. Be responsive to these requests to avoid delays.

Fifth, finalize policy issuance and payment. Review the final policy documents carefully, ensuring all agreed coverages appear correctly and exclusions match your understanding. Verify that navigation limits, crew requirements, and any special conditions align with your operational needs. Arrange payment and confirm the exact coverage effective date before taking your yacht out.

Maintaining your policy requires ongoing attention to avoid disputes and coverage gaps. Insurers are seeking to void a $2 million yacht insurance policy due to late notice and alleged breaches of policy terms, demonstrating how procedural failures can jeopardize coverage when you need it most. Timely incident reporting, accurate information updates, and compliance with policy conditions protect your coverage.

Professional crew management significantly reduces insurance risks and claims. Yachts managed by licensed captains or trained crew experience dramatically fewer insurance claims. Even if you’re an experienced owner operator, employing professional crew for complex maneuvers, challenging weather, or unfamiliar waters demonstrates prudent risk management that insurers recognize and often reward with better rates.

Familiarize yourself with the complete yacht registration guide to ensure your vessel documentation remains current alongside your insurance coverage. Many policies require proof of valid registration, and lapses can provide insurers grounds to deny claims. Exploring comprehensive boat insurance options helps you understand the full range of protection available.

Pro Tip: Schedule an annual policy review each year, ideally 60-90 days before renewal. Assess whether your coverage limits still match your yacht’s current value, review any upgrades or modifications that might affect coverage, and adjust your cruising plans or operational details. This proactive approach prevents coverage gaps and often identifies opportunities to reduce premiums through improved safety systems or operational changes.

Secure your yacht’s future with expert registration and insurance services

Navigating yacht insurance complexities becomes significantly easier when you work with specialists who understand both coverage requirements and registration compliance. Vessel Flag brings deep expertise in yacht registration and insurance coordination, streamlining the entire process while ensuring you obtain comprehensive protection tailored to your specific needs.

Our team guides you through every step, from initial yacht registration requirements to securing appropriate insurance coverage that matches your vessel type and cruising plans. We coordinate with leading maritime insurers, help you understand policy options, and ensure your documentation meets all regulatory requirements. Whether you’re registering a new yacht or reviewing existing coverage, our comprehensive approach minimizes your effort while maximizing your protection. Explore our boat insurance options and discover how Vessel Flag’s services can simplify yacht ownership while providing peace of mind on the water.

Frequently asked questions

What is covered under a standard yacht insurance policy?

Standard policies cover hull and attached equipment damage, personal belongings stored aboard, medical payments for passenger injuries, liability for third-party property damage or bodily injury, and wreck removal costs. Most policies use agreed-value coverage, guaranteeing full reimbursement up to the established vessel value without depreciation disputes.

How do yacht insurance deductibles affect my claim costs?

Deductibles represent the amount you pay out of pocket before insurance coverage begins, typically calculated as 1-3% of your yacht’s insured hull value. On a $2 million yacht with a 2% deductible, you’d pay the first $40,000 of any claim yourself. Named storm deductibles run higher at 5-10%, significantly increasing your financial exposure for hurricane damage.

Why do I need protection and indemnity insurance?

P&I insurance covers complex third-party liabilities that standard yacht policies exclude or severely limit, including environmental pollution damage, cargo damage, war and piracy risks, and comprehensive crew injury claims. These exposures can generate catastrophic financial losses, making P&I coverage essential for larger yachts, those with professional crew, or vessels cruising internationally.

What documents are required to get yacht insurance?

Insurers typically require a current marine survey from an accredited surveyor, comprehensive maintenance records demonstrating proper vessel care, and proof of ownership through title documents or purchase agreements. Additional requirements may include captain credentials for professional operators, safety equipment inventories, and detailed photographs showing the yacht’s current condition and installed systems.