TL;DR:

- Repair costs for damaged vessels are rising rapidly, making insurance essential to protect against significant financial exposure. Vessel insurance covers hull damage, liability, theft, salvage, and helps fulfill legal and port requirements for safe, responsible boat ownership. Regular policy reviews aligned with increasing repair costs and compliance ensure owners stay protected and operational across international waters.

Repair costs for damaged vessels have been climbing faster than most owners expect, and the financial exposure from a single serious incident can easily exceed the value of the boat itself. Marine insurers use empirical data and loss experience indices to price hull insurance, which means premiums reflect real and growing risks, not arbitrary fees. Whether you’re cruising domestic waters or sailing into a foreign port for the first time, vessel insurance is no longer a background formality. It’s the foundation of responsible, financially sound boat ownership, and this guide will show you exactly why and how to use it.

جدول المحتويات

- What is vessel insurance and why does it matter?

- Key benefits of vessel insurance for boat owners

- Mandatory vs. recommended: Legal and regulatory drivers

- How vessel insurance adapts to changing costs and risks

- Common mistakes and expert tips for vessel insurance

- Why the real value of vessel insurance is proactive risk management

- Streamline your compliance and insurance with Vessel Flag

- Frequently asked questions

الوجبات الرئيسية

| نقطة | التفاصيل |

|---|---|

| Insurance reduces financial risk | Vessel insurance protects you from costly loss, liability, and operational disruption. |

| Compliance varies globally | Legal requirements for insurance change by country, marina, and financing partner. |

| Policy reviews are critical | Annual or event-driven policy reviews keep your coverage aligned with real-world risks and costs. |

| Updated coverage prevents shortfalls | Keeping your insurance up to date shields you from rising repair costs and regulatory changes. |

What is vessel insurance and why does it matter?

Vessel insurance is a policy that protects your boat, your finances, and third parties against losses that arise from operating on the water. Think of it as the marine equivalent of auto or property insurance, but with a wider range of exposures that includes everything from storm damage at anchor to liability for a collision injuring another boater.

Coverage typically falls into four major categories:

- Hull and machinery: Physical damage to the boat itself, including structural repairs, machinery replacement, and salvage costs.

- Third-party liability: Financial protection if you injure someone or damage another vessel or property.

- Personal property and equipment: Covers onboard electronics, tender, safety gear, and other equipment.

- Crew and passenger protection: Medical expenses, injury, and sometimes life coverage for people aboard.

Who actually needs vessel insurance? The honest answer is almost anyone who operates a boat. Private boaters with recreational vessels face collision, theft, and weather risks daily. Commercial operators carry heavier liability exposure because paying passengers and cargo add legal complexity. Owners planning international voyages face the additional layer of foreign regulatory requirements and port entry rules that sometimes mandate proof of coverage.

The financial math is straightforward and sobering. Global marine insurance premiums reached USD 39.92 billion in 2024, with ocean hull premiums rising 3.5% from 2023 alone. That premium growth reflects real and escalating claims. One uninsured total loss event can wipe out years of savings.

Statistic callout: The global marine insurance market hit nearly USD 40 billion in premiums in 2024. That number exists because the risks are real, frequent, and expensive.

When it comes to protecting your investment, insurance isn’t the only piece of the puzzle, but it is the piece that keeps every other investment from being wiped out in a single bad day on the water. Lenders who finance vessels almost always require coverage as a loan condition. Many marinas include insurance proof in their slip agreements. And if you’re flying an international flag, your yacht insurance coverage essentials may be dictated in part by the flag state’s own compliance framework.

Pro Tip: Schedule an insurance review every time you make a significant change to your vessel, whether that’s a refit, a new engine, or a change in how you use the boat commercially. Policies written for recreational use often exclude commercial activity entirely.

Key benefits of vessel insurance for boat owners

Knowing what vessel insurance is, let’s explore what these policies actually do for you in practice.

The practical benefits go well beyond the obvious protection against accidents. Here are the core ways vessel insurance pays off for boat owners and operators:

Financial recovery after accidents. Collisions, grounding, and storm damage are among the most common and costly marine events. A single collision involving structural damage, salvage, and liability claims can run into six figures. Insurance converts that catastrophic exposure into a manageable deductible.

Protection from liability claims. If your boat injures a swimmer, damages a dock, or causes an oil spill, you’re exposed to civil legal liability that can be significant. Marine liability coverage steps in to pay defense costs and settlements, so your personal assets aren’t on the line.

Coverage for theft, fire, and total loss. Theft of outboard motors, electronics, and even entire vessels is more common than most owners realize. Fire is one of the leading causes of total loss in recreational boating. Insurance covers these losses directly.

Salvage and wreck removal. If your vessel sinks in a busy channel or near a protected marine area, local authorities may require you to remove it at your expense. Salvage costs can easily exceed the original boat value. A proper policy includes these costs.

Access to global cruising. Many foreign ports, marinas, and anchorages require proof of third-party liability insurance before they’ll allow entry. Without it, you’re simply turned away or fined, sometimes in a port you’ve just crossed an ocean to reach.

Better financing terms. Banks and marine lenders typically offer better terms when you carry adequate coverage because their collateral is protected. This can mean lower rates or more flexible conditions on your boat loan.

The rising cost of setting up vessel insurance is itself a signal worth paying attention to. Repair costs rise with macroeconomic trends like steel prices and labor rates, which means a policy you bought three years ago may be covering only a fraction of today’s actual repair bill.

“Coverage needs and claims evolve as repair costs rise with macroeconomic trends like steel prices and labor rates.” — IUMI Hull Inflation Index

Pro Tip: Don’t let outdated policy limits leave you underinsured as repair costs continue to climb. If your vessel was valued at $150,000 three years ago and comparable repairs now cost 20% more, your policy limit needs to reflect that reality or you’ll absorb the gap out of pocket.

Mandatory vs. recommended: Legal and regulatory drivers

Beyond personal financial risk, there’s also the matter of legal requirements and what happens if you travel between different jurisdictions.

The regulatory picture for vessel insurance is genuinely uneven across the world, and that unevenness catches owners off guard. Some jurisdictions don’t require boat insurance at all, while others mandate specific coverage types and minimums. What adds complexity is that even in places where national law doesn’t require it, individual marinas, lenders, or port authorities often do.

| Scenario | Insurance status | Notes |

|---|---|---|

| US domestic waters (most states) | Recommended, not always mandated | Lenders and marinas usually require it |

| European Union waters | Often required for port entry | Third-party liability frequently mandatory |

| Charter operations (worldwide) | Mandatory | Commercial use creates strict liability |

| International flag registration | Often required by flag state | Varies by flag state rules |

| Marine mortgage / boat loan | Mandatory | Lender requires hull coverage as loan condition |

Commercial and fleet operators face the strictest requirements almost universally. If you’re carrying paying passengers, running charters, or operating a commercial fishing vessel, most jurisdictions classify this as a regulated activity with mandatory liability minimums. Ignoring those requirements doesn’t just put you at financial risk. It exposes you to vessel seizure, operating license revocation, and personal legal liability.

Avoiding underinsurance and legal pitfalls requires knowing the rules in every jurisdiction where you operate, not just your home port. Yacht compliance requirements often include insurance as a component, making registration and coverage two sides of the same coin.

Key consequences of sailing uninsured where coverage is required include:

- Denial of port entry or marina berth

- Fines and penalties from port state control authorities

- Personal liability with no financial backstop for injury or property damage claims

- Vessel detention pending proof of coverage or bond posting

- Loan default if your lender discovers lapsed coverage

Review boat insurance requirements by location before planning any international passage to avoid surprises at customs or in port.

How vessel insurance adapts to changing costs and risks

Understanding the law is just one part. Let’s see how market forces and rising costs reshape what insurance covers and costs year by year.

The IUMI Hull Inflation Index is one of the clearest tools available for understanding how real-world economics drive marine insurance. Policy pricing aligns with drivers like steel prices, wages, and shipyard capacity, and owners who don’t account for this in their annual policy review risk being significantly underinsured within just a few years.

| Cost driver | Impact on insurance claims | Trend (2022 to 2026) |

|---|---|---|

| Steel and aluminum prices | Higher hull repair costs | Elevated, volatile |

| Skilled marine labor rates | Increased repair labor costs | Rising steadily |

| Shipyard capacity constraints | Longer repair times, higher costs | Capacity tightening |

| Electronic and navigation equipment | Growing replacement value | Increasing rapidly |

| Environmental compliance costs | Wreck removal and pollution expenses | Rising with regulation |

The practical implication is significant. A vessel insured for its purchase value five years ago may be insured at 60 to 70 percent of its current replacement or repair cost. That gap is entirely invisible until a claim happens, and then it becomes very visible, very quickly.

Commercial vessel registration often has its own valuation requirements tied to the registration flag, which is one more reason why registration and insurance need to be reviewed together rather than treated as separate tasks.

Pro Tip: Schedule a formal annual policy review every year at renewal time. Bring your insurer updated valuations for the hull and all major equipment, especially electronics, which depreciate rapidly in the market but cost significantly more to replace than their depreciated value.

Common mistakes and expert tips for vessel insurance

With this understanding, let’s finish with a set of actionable steps and expert advice for making your coverage work best for you.

The most expensive vessel insurance mistakes are almost always avoidable. They typically come from inattention rather than ignorance. Here are the most common errors and what to do instead:

Assuming coverage is optional. Many owners skip insurance until a marina, lender, or foreign port forces the issue. By that point, you’re buying coverage under pressure rather than on good terms.

Underinsuring vessel value. Insuring for purchase price rather than current replacement value is the single most common and costly mistake in marine insurance. Repair cost inflation makes this gap worse every year.

Missing compliance rules for new travel destinations. Owners who sail into new waters, especially internationally, often don’t check the insurance requirements specific to that jurisdiction until they’re already there.

Forgetting to review annually. A policy that was adequate when you bought it may be inadequate now. Periodic review and adjustment of insurance coverage protects owners from underinsurance as market rates and repair costs shift.

Using recreational policies for commercial activity. If you charge passengers or run any form of paid service on your vessel, a recreational policy is likely to void your coverage for those activities.

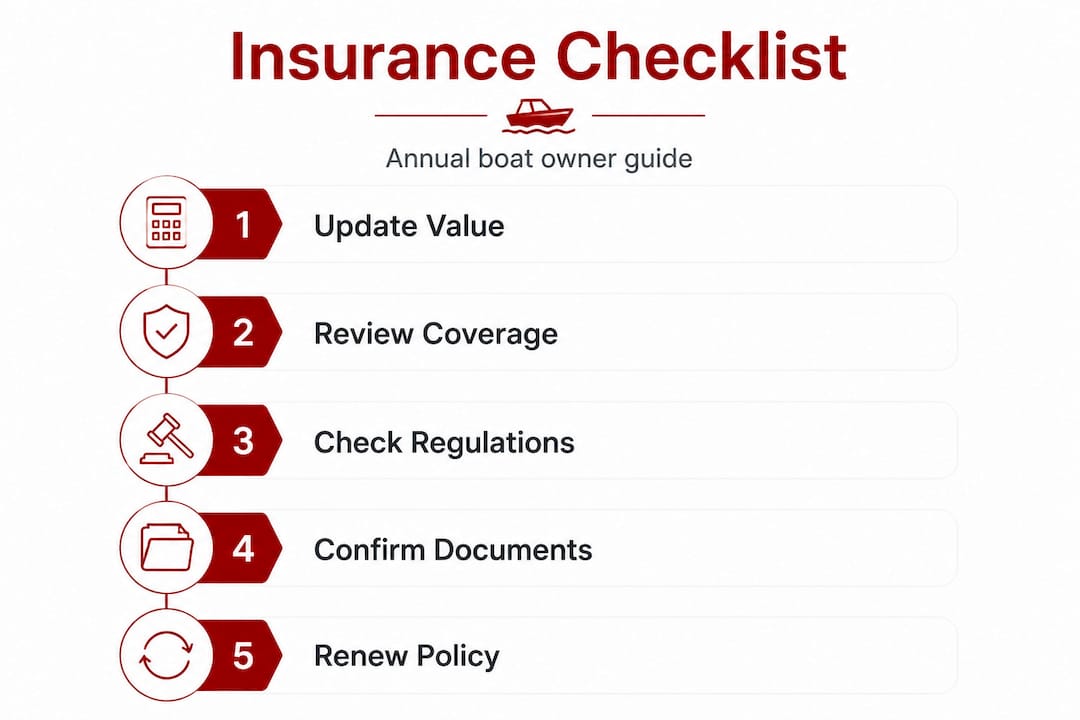

Your annual insurance review checklist should include:

- Confirm current vessel market value and compare to insured value

- Review policy limits for liability, especially if usage has expanded

- Check coverage geography matches your planned cruising area

- Verify crew and passenger coverage if applicable

- Confirm the policy aligns with any current registration and flag state requirements

- Ask your broker about any relevant changes in port entry insurance requirements for your destinations

Exploring vessel insurance options before you need coverage is always a better strategy than scrambling when a marina or port authority asks for proof.

Pro Tip: Work with an insurance agent who has specific experience with international marine regulations if you plan to cruise outside your home country. Generic marine insurers may not understand the compliance nuances of flag state requirements or port entry rules in your destinations.

Why the real value of vessel insurance is proactive risk management

Most owners think about vessel insurance as a one-time requirement. You buy the policy, pay the premium each year, and move on. The real lesson from decades of watching how claims and compliance issues unfold is that this passive approach is where most of the financial pain comes from.

83% of observed variance in hull insurance claims can be explained by real-world economic drivers. That number is striking because it means most claim severity outcomes aren’t random, they’re predictable given what’s happening in the broader economy. If steel prices are up, shipyard labor is tight, and electronics replacement costs have risen, your claims exposure is measurably higher this year than it was two years ago, even if nothing about your vessel has changed.

The owners who manage this reality well don’t just renew their policies. They treat insurance as risk management infrastructure, the same way a business treats its liability policies. They review limits against current costs. They check their policy scope against their actual usage and cruising plans. They ask their broker hard questions about whether their coverage would actually make them whole in a total loss scenario.

The other thing most articles miss is the opportunity side of proper insurance. Well-documented coverage at adequate limits opens doors. You get better financing terms. Marinas and ports accept you without friction. You gain access to foreign anchorages and commercial berths that turn away uninsured vessels. Insurance is not just protection against loss. It’s a credential that expands your operational range.

Treat your policy like a business asset. Review it, adapt it as your situation changes, and don’t let the comfort of having any policy stop you from asking whether it’s actually the right policy for where you’re going and what you’re doing now.

Streamline your compliance and insurance with Vessel Flag

If the connection between registration, flag state compliance, and vessel insurance feels like a lot to manage, you’re not wrong. These three elements have to work together, and gaps in any one of them can create problems in the others.

موقع VesselFlag.com helps yacht owners and boat operators navigate exactly this intersection. From helping you understand yacht vs boat registration requirements to ensuring yacht registration validity across multiple jurisdictions, the platform brings together registration services, insurance guidance, and compliance support in one place. Whether you need a flag that aligns with your cruising area or want to confirm your coverage meets port entry requirements, موقع VesselFlag.com gives you the expertise and the tools to get it right from the start. Take the next step toward fully compliant, fully protected vessel operations.

Frequently asked questions

Is vessel insurance required everywhere?

No, not all countries require vessel insurance by law, but marinas, lenders, or international travel often make it mandatory or highly recommended regardless of national rules.

How often should I review my vessel insurance policy?

Review your vessel insurance at least annually, and also whenever vessel value, usage, or market repair costs change substantially enough to affect what your policy would actually pay out.

Does vessel insurance cover international operations?

Many vessel insurance policies include international coverage, but terms vary widely by insurer, flag state, and destination. Always confirm geographic scope and compliance requirements before departure.

What is the biggest risk of not having vessel insurance?

Without coverage, you face direct financial exposure from accidents and liability claims, and you may be barred from port entry or face vessel detention. Real and rising claim costs mean uninsured losses are more severe than most owners anticipate.