TL;DR:

- Vessel insurance is legally required in many jurisdictions to operate internationally and commercially.

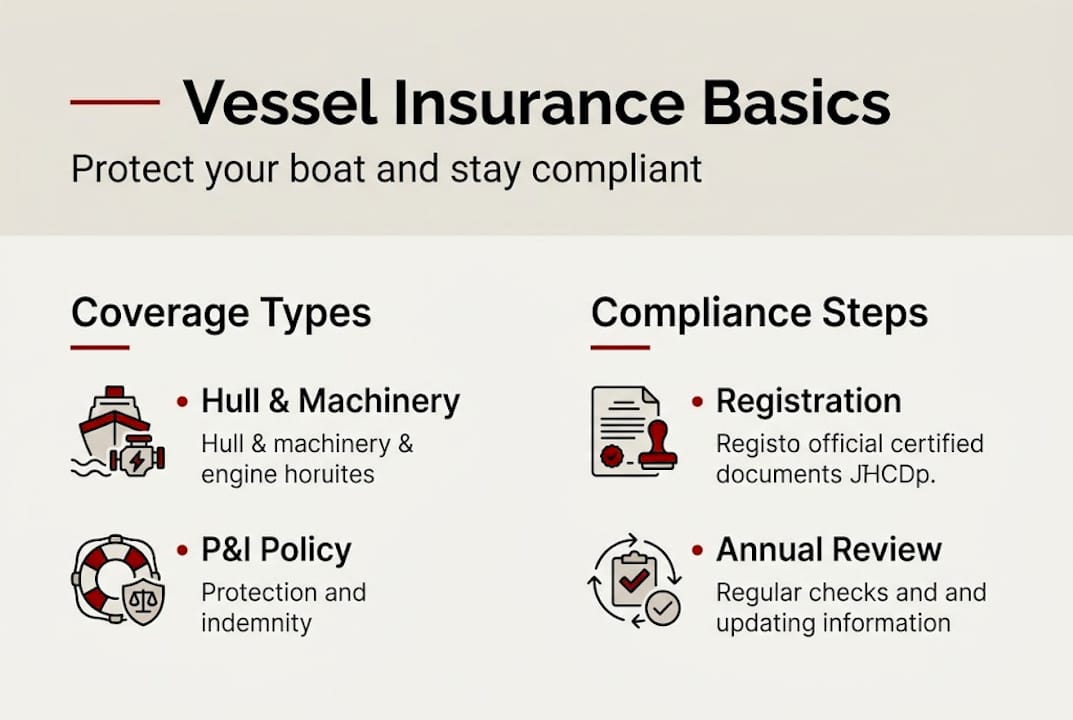

- It consists of Hull & Machinery coverage for vessel damage and Protection & Indemnity for third-party liabilities.

- Regularly reviewing and updating policies ensures compliance and protects against financial and legal risks.

Most yacht and boat owners treat vessel insurance the way they treat a life jacket: something they hope they never need. But this thinking misses the point entirely. In most international waters and ports, operating without proper insurance isn’t just risky, it’s illegal. Vessel insurance is both a regulatory requirement and a financial shield, and the two roles are inseparable. Whether you’re sailing the Mediterranean on a private yacht or running a commercial vessel in Caribbean waters, understanding how coverage works protects your investment, your crew, and your license to operate.

جدول المحتويات

- What is vessel insurance and why does it matter?

- How vessel insurance enables global compliance

- Evaluating coverage: Choosing policies for your vessel’s needs

- Claims, risks, and pitfalls: What owners often overlook

- Our perspective: What most owners get wrong about vessel insurance

- Get expert help securing vessel insurance and compliance

- Frequently asked questions

الوجبات الرئيسية

| نقطة | التفاصيل |

|---|---|

| Covers legal and financial risks | Vessel insurance protects owners from costly accidents and liability claims. |

| Ensures compliance | Proper insurance is required for vessel registration and operation in most countries. |

| Choose tailored policies | Select insurance coverage based on vessel type, use, and operational area. |

| Update policies regularly | Review and adjust insurance as your boat use or regulations change. |

What is vessel insurance and why does it matter?

At its core, vessel insurance is a contractual arrangement between a vessel owner and an insurer to manage the financial risks that come with owning and operating a boat or yacht. It isn’t one-size-fits-all. Most marine insurance structures fall into two main categories: Hull & Machinery (H&M) and Protection & Indemnity (P&I). Understanding each is essential before you sign anything.

Vessel insurance primarily consists of Hull & Machinery covering physical damage to the vessel and Protection & Indemnity covering third-party liabilities. Here’s what that means in practice:

- H&M coverage protects your vessel itself. Think collision with another boat, grounding on a reef, fire damage, storm damage, and even theft. If the physical structure or machinery of your vessel is harmed, H&M is what pays for repairs or replacement.

- P&I coverage handles the fallout that affects others. Crew injury claims, pollution liability, cargo damage, and even the cost of wreck removal after a sinking all fall here. Without P&I, you’re personally exposed to claims that could run into the millions.

- Exclusions matter. Wear and tear, manufacturer defects, and intentional damage are typically excluded. Most policies also exclude losses from operating outside your agreed geographic limits.

“Vessel insurance is not just a financial product, it is a prerequisite for responsible maritime operation. Knowing the difference between what H&M covers and what P&I handles can mean the difference between a resolved claim and a financial catastrophe.”

You can explore yacht insurance essentials in detail to understand how each coverage type applies to your specific situation. Many owners make the mistake of assuming any policy covers everything, but gaps between H&M and P&I are exactly where expensive surprises hide.

For practical setup guidance, the boat insurance setup process helps clarify what documentation and declarations are needed from day one. Getting this right at the start saves significant headaches during a claim.

How vessel insurance enables global compliance

Knowing what vessel insurance covers is only half the picture. The other half is understanding that in most jurisdictions, you simply cannot operate without it. Vessel insurance is essential for complying with international maritime regulations, and requirements differ significantly from one region to the next.

Here’s a comparison of insurance requirements across major maritime jurisdictions:

| Jurisdiction | Minimum Insurance Required | Notes |

|---|---|---|

| European Union | P&I mandatory for commercial vessels | Recreational vessels vary by member state |

| United States | No federal mandate, but marina/port access often requires it | State laws and lender requirements apply |

| Caribbean | Required for most charter and commercial operations | Varies by island nation |

| Mediterranean | P&I often required for port entry | Flag state rules apply |

| UK Waters | P&I required for commercial operations | Recreational boats recommended |

Failing to carry the right insurance doesn’t just expose you to financial risk. It can result in denied port entry, fines, confiscation of your vessel, or outright revocation of your registration. Many port authorities in the EU and Caribbean actively check insurance documentation before granting berth access.

Here’s how to keep your vessel compliant across jurisdictions:

- Secure appropriate H&M and P&I policies before registering or operating in any jurisdiction.

- Match your coverage to regulatory minimums in each country or region where you plan to operate.

- Review flag state requirements since the country where your vessel is registered may impose additional insurance conditions.

- Update your insurer whenever you change your area of operation, add crew, or alter the vessel’s commercial status.

- Keep documentation current and accessible. Port inspectors can request proof of insurance at any time.

Understanding vessel registration requirements is closely tied to insurance compliance. Registration and insurance are reviewed together in many jurisdictions, meaning a lapse in one can invalidate the other. Use a vessel registration guide to stay aligned with current 2026 regulations.

Evaluating coverage: Choosing policies for your vessel’s needs

Compliance sets the floor. But the right policy for your vessel goes beyond the minimum. H&M and P&I policies can be customized to the vessel’s usage, value, and operator profile, so the goal is finding coverage that genuinely fits your operation.

Here’s how coverage needs shift depending on your situation:

| Scenario | Key Coverage Priority | Considerations |

|---|---|---|

| Private yacht, Mediterranean | H&M with broad geographic scope | Seasonal coverage options may reduce cost |

| Charter yacht, Caribbean | P&I with passenger liability | High liability limits essential |

| Commercial vessel, EU | Full H&M and P&I, crew coverage | Manning certificates often required |

| Coastal recreational boat | Basic H&M | Liability add-ons recommended |

Several factors determine what you’ll pay and what you’ll be covered for:

- Vessel age and condition: Older vessels often face higher premiums or stricter survey requirements.

- Size and value: Larger, more expensive vessels require proportionally higher coverage limits.

- Area of operation: Offshore and international routes carry higher risk than inland waters.

- Crew requirements: Commercial operations with hired crew trigger additional P&I considerations.

- Usage type: Private versus charter versus commercial use each carry different legal exposures.

When comparing policies, check for these features:

- Agreed value versus market value settlement (agreed value is better for owners)

- Geographic coverage limits and any navigation warranties

- Wreck removal and pollution liability sublimits

- Crew personal accident coverage inclusion

- Salvage coverage and towing assistance

Pro Tip: Review your policy at least once a year. If you’ve changed your cruising area, started chartering, or added crew, your existing policy may no longer adequately protect you. Avoiding underinsurance pitfalls requires active management, not just an annual premium payment.

For a structured breakdown of what a sound policy should include, the yacht insurance policy essentials guide is a strong starting point.

Claims, risks, and pitfalls: What owners often overlook

Choosing a policy is only the beginning. Knowing how to use it when something goes wrong separates owners who recover quickly from those who face prolonged disputes or denied claims. Accidents covered include collision, grounding, fire, and third-party liabilities, but the claims process for each can look very different.

Here’s how a typical claim unfolds:

- Notify your insurer immediately after an incident. Delayed reporting is one of the most common reasons claims are complicated or denied.

- Document everything. Photographs, witness statements, official incident reports, and AIS logs all support your case.

- Cooperate with the surveyor. Your insurer will likely send a marine surveyor to assess damage. Prepare your vessel and records accordingly.

- Submit all required forms within the timeframes specified in your policy. Missing a deadline can void your claim.

- Follow the resolution process. Claims may take weeks to months depending on complexity, especially for major damage or third-party disputes.

Most overlooked risks vessel owners face:

- Operating outside navigation limits: Your policy likely defines where your vessel is covered. Cross that line and coverage disappears.

- Unreported modifications: Adding a generator, changing propulsion, or converting for charter use without telling your insurer can void your coverage.

- Ignoring crew changes: Hiring an unlicensed captain or adding temporary crew without updating your P&I policy creates liability exposure.

- Letting policies lapse during lay-up: Vessels in storage still face fire, theft, and weather risks. Lay-up clauses should keep basic coverage active.

Pro Tip: Keep a vessel logbook with maintenance records, crew certifications, and incident notes. This documentation is invaluable if a claim is ever contested. A well-maintained log shows the insurer that the vessel was properly managed before the loss occurred.

For detailed information on what different التأمين على القوارب structures include, reviewing policy documents alongside expert guidance pays off when it matters most.

Our perspective: What most owners get wrong about vessel insurance

After working with yacht owners and operators across dozens of flag states, the pattern is consistent: most people treat vessel insurance as a checkbox. Buy the policy, file it away, renew it once a year without looking at it. That approach works right up until it doesn’t.

The real risk isn’t an uninsured vessel. It’s a vessel that’s technically insured but effectively unprotected because the policy hasn’t kept pace with how the vessel is actually being used. We’ve seen owners denied claims because they quietly started occasional charter operations without updating their coverage. Others discovered their geographic limit excluded the exact waters where they suffered a loss.

The uncomfortable truth is that insurance strategy should evolve with your vessel operations, not stay static. Review your coverage every time your circumstances change. If you’re unsure whether a change in use triggers a policy update, ask your broker before the incident happens. Understanding boat underinsurance risks isn’t alarmist thinking. It’s how experienced owners stay protected.

True marine risk management means negotiating for policy flexibility and keeping your insurer informed. Compliance is the floor, not the ceiling.

Get expert help securing vessel insurance and compliance

Navigating vessel insurance requirements across multiple jurisdictions is genuinely complex, and the cost of getting it wrong is high. If you want direct support to make the process seamless, working with specialists who understand both maritime compliance and registration requirements gives you a clear advantage.

موقع VesselFlag.com provides guidance across the full spectrum of vessel ownership needs. Start with the yacht registration guide to understand how registration and insurance intersect, then explore yacht compliance essentials to make sure your operation meets 2026 regulatory standards. When you’re ready to secure coverage, get a boat insurance quote tailored to your vessel’s profile and operational area. Expert guidance removes the guesswork and keeps your investment protected.

Frequently asked questions

What does vessel insurance typically cover?

Vessel insurance usually includes Hull & Machinery for damage to your own vessel and Protection & Indemnity for third-party liabilities such as crew injury, pollution, and wreck removal.

Is vessel insurance required by law?

Many countries require vessel insurance for registration or port access, particularly for commercial vessels. Most international jurisdictions require proof of insurance before granting operational permits.

How is a vessel insurance claim processed?

After an incident, notify your insurer immediately, document the damage thoroughly, cooperate with the appointed surveyor, and submit all forms within your policy’s deadlines. Covered accidents include collision, grounding, and fire.

What happens if I don’t update my vessel insurance policy as required?

Your claim could be denied, or your vessel may be found non-compliant with local laws. Lack of proper insurance can result in penalties, port denial, or forfeiture of registration.

Can vessel insurance be customized for international operations?

Yes. H&M and P&I policies can be tailored to your specific routes, vessel type, crew profile, and the regulatory requirements of each country where you operate.